时间序列预测之 AUTO-ARIMA

作者:互联网

参考链接:常用7种时间序列预测模型

运用ARIMA进行时间序列建模的基本步骤:

- 1)加载数据:构建模型的第一步当然是加载数据集。

- 2)预处理:根据数据集定义预处理步骤。包括创建时间戳、日期/时间列转换为d类型、序列单变量化等。

- 3)序列平稳化:为了满足假设,应确保序列平稳。这包括检查序列的平稳性和执行所需的转换。

- 4)确定d值:为了使序列平稳,执行差分操作的次数将确定为d值。

- 5)创建ACF和PACF图:这是ARIMA实现中最重要的一步。用ACF PACF图来确定ARIMA模型的输入参数。

- 6)确定p值和q值:从上一步的ACF和PACF图中读取p和q的值。

- 7)拟合ARIMA模型:利用我们从前面步骤中计算出来的数据和参数值,拟合ARIMA模型。

- 8)在验证集上进行预测:预测未来的值。

- 9)计算RMSE:通过检查RMSE值来检查模型的性能,用验证集上的预测值和实际值检查RMSE值。

ARMA模型公式:

信息准则定阶

- AIC(Akaike Information Criterion)

L是数据的似然函数,k=1表示模型考虑常数c,k=0表示不考虑。最后一个1表示算上误差项,所以其实第二项就是2乘以参数个数。

- AICc(修正过的AIC)

- BIC(Bayesian Information Criterion)

注意事项:

- 信息准则越小,说明参数的选择越好,一般使用AICc或者BIC。

- 差分d,不要使用信息准则来判断,因为差分会改变了似然函数使用的数据,使得信息准则的比较失去意义,所以通常用别的方法先选择出合适的d。

- 信息准则的好处是可以在用模型给出预测之前,就对模型的超参做一个量化评估,这对批量预测的场景尤其有用,因为批量预测往往需要在程序执行过程中自动定阶。

模型构建

from statsmodels.tsa.arima_model import ARIMA # 1,1,2 ARIMA Model model = ARIMA(df.value, order=(1,1,2)) model_fit = model.fit(disp=0) print(model_fit.summary())

中间的表格列出了训练得到的模型各项和对应的系数,如果系数很小,且‘P>|z|’ 列下的P-Value值远大于0.05,则该项应该去掉,比如左图中的ma部分的第二项,系数是-0.0010,P-Value值是0.998,那么可以重建模型为ARIMA(1,1,1),从右图可以看到,修改阶数后的模型的AIC等信息准则都有所降低:

通常会检查模型拟合的残差序列,即训练数据原本的序列减去训练数据上的拟合序列后的序列。该序列越符合随机误差分布(均值为0的正态分布),说明模型拟合的越好,否则,说明还有一些因素模型未能考虑。

# Plot residual errors residuals = pd.DataFrame(model_fit.resid) fig, ax = plt.subplots(1,2) residuals.plot(title="Residuals", ax=ax[0]) residuals.plot(kind='kde', title='Density', ax=ax[1]) plt.show() # Actual vs Fitted model_fit.plot_predict(dynamic=False) plt.show()

from statsmodels.tsa.stattools import acf

# Create Training and Test

train = df.value[:85]

test = df.value[85:]

# Build Model

model = ARIMA(train, order=(3,2,1))

# model = ARIMA(train, order=(1, 1, 1)) #预测效果很差,选用上面的效果有提升

fitted = model.fit(disp=-1)

# Forecast

fc, se, conf = fitted.forecast(15, alpha=0.05) # 95% conf

# Make as pandas series

fc_series = pd.Series(fc, index=test.index)

lower_series = pd.Series(conf[:, 0], index=test.index)

upper_series = pd.Series(conf[:, 1], index=test.index)

# Plot

plt.figure(figsize=(12,5), dpi=100)

plt.plot(train, label='training')

plt.plot(test, label='actual')

plt.plot(fc_series, label='forecast')

plt.fill_between(lower_series.index, lower_series, upper_series,

color='k', alpha=.15)

plt.title('Forecast vs Actuals')

plt.legend(loc='upper left', fontsize=8)

plt.show()

AUTO-ARIMA模型 (python - pmdarima;r - forecast)

通过预测结果来推断模型阶数的好坏毕竟还是耗时耗力了些,一般可以通过计算AIC或BIC的方式来找出更好的阶数组合。pmdarima模块的auto_arima方法就可以让我们指定一个阶数上限和信息准则计算方法,从而找到信息准则最小的阶数组合。

from statsmodels.tsa.arima_model import ARIMA

import pmdarima as pm

df = pd.read_csv('https://raw.githubusercontent.com/selva86/datasets/master/wwwusage.csv', names=['value'], header=0)

model = pm.auto_arima(df.value, start_p=1, start_q=1,

information_criterion='aic',

test='adf', # use adftest to find optimal 'd'

max_p=3, max_q=3, # maximum p and q

m=1, # frequency of series

d=None, # let model determine 'd'

seasonal=False, # No Seasonality

start_P=0,

D=0,

trace=True,

error_action='ignore',

suppress_warnings=True,

stepwise=True)

print(model.summary())

# Forecast

n_periods = 24

fc, confint = model.predict(n_periods=n_periods, return_conf_int=True)

index_of_fc = np.arange(len(df.value), len(df.value)+n_periods)

# make series for plotting purpose

fc_series = pd.Series(fc, index=index_of_fc)

lower_series = pd.Series(confint[:, 0], index=index_of_fc)

upper_series = pd.Series(confint[:, 1], index=index_of_fc)

# Plot

plt.plot(df.value)

plt.plot(fc_series, color='darkgreen')

plt.fill_between(lower_series.index,

lower_series,

upper_series,

color='k', alpha=.15)

plt.title("Final Forecast of WWW Usage")

plt.show()

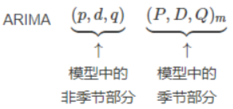

如何自动构建季节性ARIMA模型?

如果模型带有季节性,则除了p,d,q以外,模型还需要引入季节性部分:

与非季节性模型的区别在于,季节性模型都是以m为固定周期来做计算的,比如D就是季节性差分,是用当前值减去上一个季节周期的值,P和Q和非季节性的p,q的区别也是在于前者是以季节窗口为单位,而后者是连续时间的。

上节介绍的auto arima的代码中,seasonal参数设为了false,构建季节性模型的时候,把该参数置为True,然后对应的P,D,Q,m参数即可,代码如下:

# !pip3 install pyramid-arima

import pmdarima as pm

# Seasonal - fit stepwise auto-ARIMA

smodel = pm.auto_arima(data, start_p=1, start_q=1,

test='adf',

max_p=3, max_q=3, m=12,

start_P=0, seasonal=True,

d=None, D=1, trace=True,

error_action='ignore',

suppress_warnings=True,

stepwise=True)

smodel.summary()

注意这里的stepwise参数,默认值就是True,表示用stepwise algorithm来选择最佳的参数组合,会比计算所有的参数组合要快很多,而且几乎不会过拟合,当然也有可能忽略了最优的组合参数。所以如果你想让模型自动计算所有的参数组合,然后选择最优的,可以将stepwise设为False。

如何在预测中引入其它相关的变量?

标签:index,plt,AUTO,模型,ARIMA,series,序列,model 来源: https://www.cnblogs.com/iupoint/p/14621830.html